Student debt and moral luck

Here’s a little story about student debt: When I decided to go to law school in the mid-1980s, I had no idea what I was doing in either purely financial terms, or for that matter professionally (I was blissfully unaware of how lawyers made a living or even really what they did). I was 25, extremely financially naive, and only vaguely aware of what going to law school might cost. This was pre-Internet, which means the kind of research you can now do on your smartphone was difficult to do, comparatively speaking.

I only applied to about five schools IIRC, because I figured if I didn’t get into a really good school it probably wasn’t worth going. This was a, loosely speaking, accurate belief in my case, but it was a product of just dumb guesswork rather than actual analysis of any sort.

Anyway I got into Michigan and decided to go there because I was already living in Ann Arbor so I could get the cheap in-state tuition, which was a little more than third of that at the top private law schools. I ended up funding my three years of law school tuition exclusively with federal student loans, because what savings I had and money I made working summers during law school all went to paying living expenses.

Tuition during my first year was $4,500, which is just under $12,000 in constant 2022 dollars. It was going up at about 10% per year at that point, so I ended up borrowing about $15,000 over the three years of law school. Six months after I graduated, this had ballooned to about $20,000 because the interest on the loans accrued during law school (I can’t remember if it compounded. It probably did, these being educational loans and all).

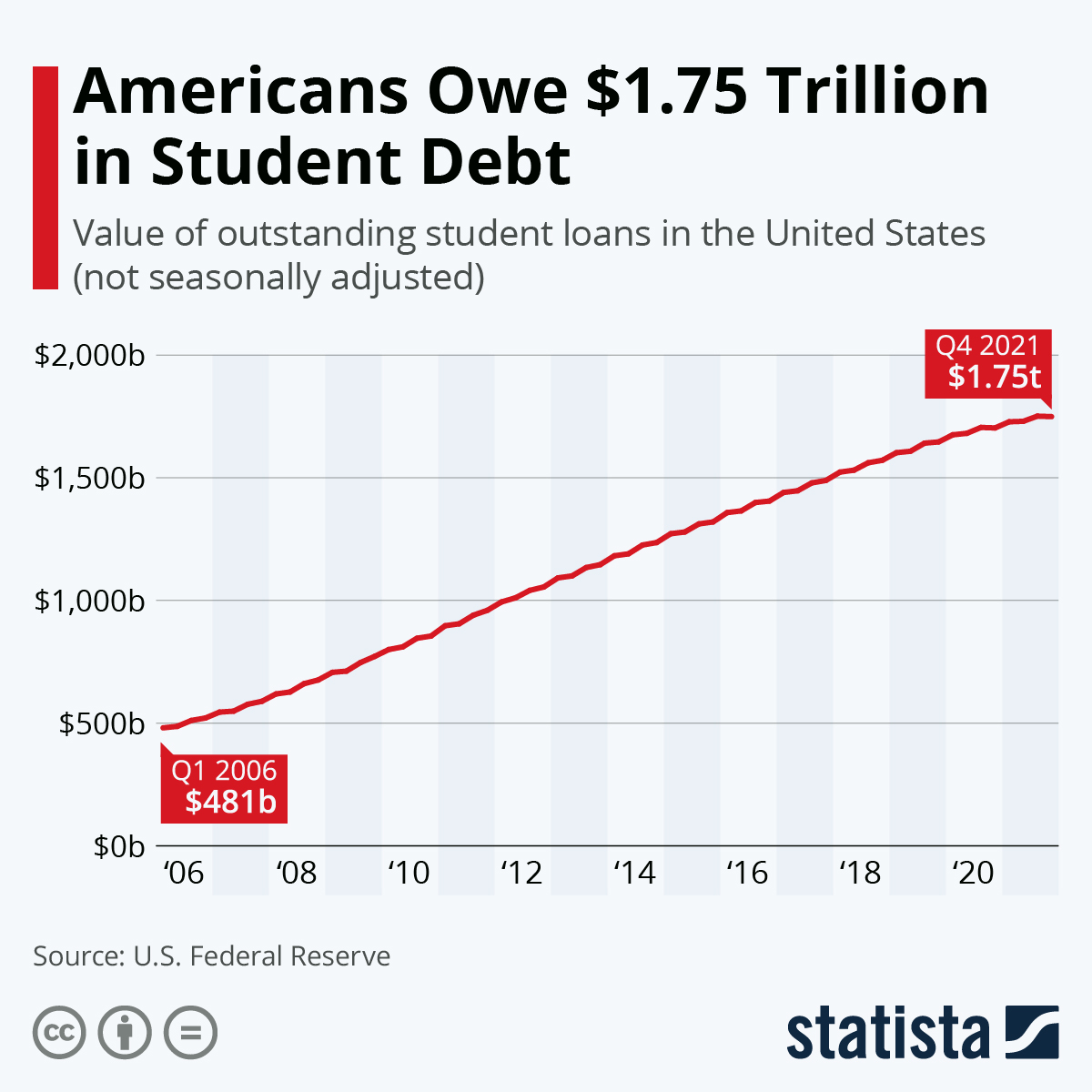

So when I made my first loan payment in the fall of 1989, I owed about $47,000 in educational debt, in 2022 dollars.

Now here’s something I didn’t know at the time: If I had been an early baby boomer, born around the same time as Donald Trump, instead of a late boomer, born near the end of that demographic, which runs between 1946 and 1964, I would have paid way less in real dollars for my three years of law school. How much less? Well if I had enrolled in the fall of 1968 instead of 1986, my tuition would have been a $620, which was the equivalent of $1900 in 1986 dollars, i.e. quite a bit less than half of the tuition I actually paid.

Indeed, during my first year of law school John Kramer, a law school dean who would also become president of the Association of American Law Schools, published an article lamenting the severe run-up in law school tuition over the previous two decades, which he noted had more than doubled in real terms. So we late boomers were really getting shafted.

Flash forward to 2022. What’s in-state tuition at Michigan’s law school now? Recall that, in constant dollars, it was about the $5,000 in 1968 and $12,000 in 1986. The answer is, just a smidge under $67,000. If the 2022 version of 25 year old me were to undertake the same excellent adventure I launched myself upon 35 years ago — again, let me emphasize that I had absolutely no idea what I was doing, either financially or professionally — I would end up borrowing not $15,000 but rather more than $200,000, meaning that six months after graduation I wouldn’t have $47,000 in debt (2022 dollars), but more like $250,000, what with all the accruing interest etc.

Yet I would have had maybe $20,000 in debt (2022 dollars) if I had gone to law school in 1968 instead of 1986.

The moral of this story, the moral of this song, is simply one should never be where one does not belong . . . wait that’s not it. The real moral here is that blaming Kids These Days for piling up educational debt is asinine on many levels, because that’s not how life works. How life works is that people who understandably have no real idea what they’re doing were dealt great cards if they were born in the mid-1940s, and goodish ones if they were born 15 years later, and terrible ones if they were born 30 years after that, and therefore ignoring the sheer randomness of moral luck is what really awful people do. For example:

“I mean paying off loans for people that don’t wanna, they wanna have some bizarre basket-weaving, you know, degree?” she said. “And they want all of us, people watching across this country, hardworking men and women, to subsidize their laziness and their inability to even try to contribute to society.”

That’s Kimberly Guifoyle, complaining about Joe Biden’s “communist” approach to student loan debt. Kim’s big career break consisted of marrying Gavin Newsom, which is one strategy for dealing with debts no honest man can pay, although she certainly went on to bigger and better things:

The former TV personality, who is engaged to Donald Trump Jr., was secretly paid $180,000 a year by the Trump campaign via the campaign manager’s private company, HuffPost reported in 2020. She was also paid $60,000 for a short speech introducing Trump Jr. at the Jan. 6, 2021 rally that led to the assault on the U.S. Capitol that was carried out by Trump supporters.

“I’m not saying it’s a crime,” Rep. Zoe Lofgren (D-Calif.) said on CNN in June about the speaking fee for a speech that lasted less than 3 minutes. “But I think it’s a grift.”

Ya think?